The path to Consolidation: The mix and matching process

Are your GICs, TFSA or fixed term RRSP deposit portfolios becoming more complicated and challenging to manage?

If managing a GIC portfolio has you concerned about:

- Miscalculating an investment rollover or interest payment date

- Too many investments issued by different bank or trust company branches

- products denominated in differing dollar amounts

- Converting RRSPs into income

- Whether you’ve received an interest payment

- Maturing at inconvenient or odd times

- Whether your investments are fully insured by CDIC

- Whether you’ve received the correct number of T5 slips, or

- Needing to re-register certain investments into “joint” registration for estate proposes

If any question rings true, perhaps it is time to consider starting the consolidation process.

Moreover, early consolidation is especially important if your RRSPs funds are to be converted into income producing RRIF accounts. In some cases this process may need a lead-time of 5 years prior to retirement.

Getting started with lots of available options – Did you know?

You can choose any particular date to have a short-term investment mature. E.g.: say, 42 days from today, or if your next maturing investment is say the 3rd of the month consider matching that maturity amount with a current investment.

By using an investment savings account as a holding tank, you can accumulate and combine your cash for reinvestment into a larger deposit, and match it up with other upcoming maturities.

Investing in a cashable GICs locks in a fixed rate while providing the option of an early redemption feature – you could have any group of cashable-GICs earmarked for redemption at a future date.

Taking steps towards consolidation:

Step 1) Assemble your investment receipts in date order, starting with the earliest maturity date. Record your investments on graph paper, under column headings such as Issuer, Amount, Interest rate, and maturity date (you might want to try out our GIC Consolidation worksheet, it may help).

Step 2) Identify and group all investments with close or matching maturity dates

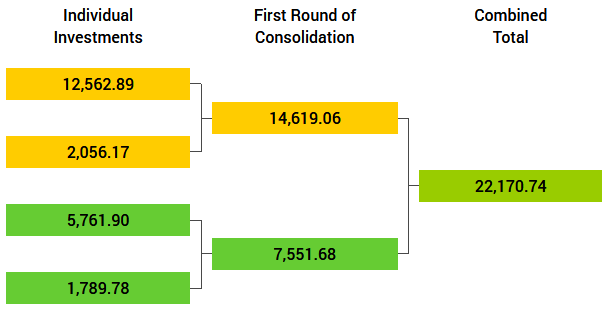

Step 3) When deciding upon certain future maturity dates and the combined dollars amounts. You may be reminded that the process is similar to a sports playoff league table. Two investments moving forward, joining two others at a future date, then on to another group of maturing investments – towards, yet another common maturity date. The result being the combination of many smaller investments into larger denominated and thus a more manageable portfolio.

Combined Individual investments into two, then one

RRSP consolidation: Use the same tactics as above, but note the accumulated compounded value as the maturing dollar amount – if need be, add an extra column to your list – recording any applicable transfer fees. Any such fees may have a detrimental effect on the investments

return. It takes a little time and some effort to transfer from one institution to another. This is accomplished by making a new application in advance of the maturing funds. Then provide instructions to the current issuer indicating to whom the funds are to be forwarded (if possible note your new account numbers in your instructions).

Retain the name of the person(s) you’ve talked with – as it’s likely you’ll need to remind them or to follow-up on your instructions. Delivering the transfer notice in person is the most prudent action.

Planning a course of action while your investments are in the RRSP stage is by far the best place to start. One important feature that registered accounts have is a “guaranteed rate period.” This period can be as long as 30 days while your money is being transferred between institutions. No interest is being earned while in transition. It’s worth remembering that institutions are notoriously slow to transfer account out.

Choosing what to invest in throughout this consolidation process is made easier by the numerous investment vehicles in the marketplace. Savings accounts, short-term deposits or one-year cashable GICs allow more flexibility, and at times a better rate. Speak with your Fiscal Agents investment advisor to determine how this will be beneficial to your fixed term retirement portfolio and how it may help you meet your financial goals. Contact us today.

Consolidating your maturing RRSPs sooner than later is one of the smartest planning and money management strategies of any GIC type of investment certificates.